")

Unique challenges for small business owners

© 2024 First Samuel Limited

Photo © Rido from Via Canva.com

A small business owner and his or her partner face a unique financial challenge: their personal wealth management issues are woven into their business. And vice-versa. This integration is not only fiscal, it is also emotional.

This distinguishes their needs from those of, say, an employee of a company or a public servant.

Many of our clients are small business owners, for example doctors who run their own private practice, or businessmen and women in retailing.

Having served such clients for more than 22 years, we know that the integration of business and personal finances presents both challenges and opportunities.

Summary

An inter-entity property transfer and other strategies substantially reduce tax.

Our clients

David and Angela have been our clients since 2005.

David, with Angela’s help, ran the family business, and had seen it grow successfully over many years. Both were passionate about the business. They have three children who are now financially independent.

The business is located south of Melbourne.

What they sought

- To accumulate investments in tax efficient structures with growth and moderate risk

- To gift or loan about $100,000 to each child to assist with property purchases

- A recommendation about the ownership of a small industrial property investment currently held by the family trust

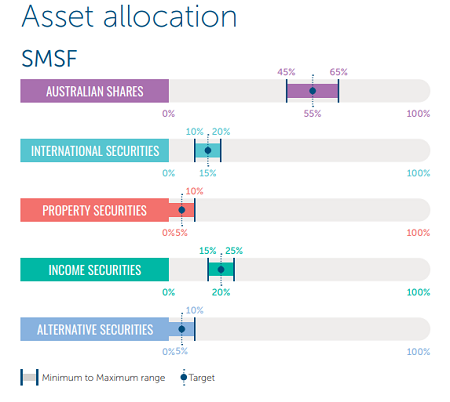

- SMSF investments diversified across a range of assets and markets

- Advice on what to do with net proceeds from the sale of their home and purchase of a smaller home

- Ongoing wealth strategy advice as their circumstances and/or government rules changed

Critical client facts

- David and Angela are business smart, but with modest investment knowledge or ability

- They have little time to manage their own investments

- Financially, their more recent and key arrangements were:

- Commercial and residential investment properties valued at over $8m

- The business generates significant surplus cash flow ($0.8m plus), but this fluctuates

- Zero debt

- They sold their family home to downsize, with a net gain of $1.5m

What we advised – summary

- Transfer the ownership of the industrial property to their SMSF, utilising the small business CGT concession

- Monitor property investments to ensure costs (e.g. land tax, fees, etc) were proportionate to revenue

- Each make the maximum ‘downsizer’ contribution ($300,000) into their SMSF

- Invest other funds ($600,000) from home downsize in a new family trust portfolio

- Maximise concessional and non-concessional superannuation contributions from surplus cash flow

What was special:

1. Property transfer to SMSF:

- reduced overall land tax of over $20,000 p.a.

- reduced tax on property rent and future CGT

- transfer costs will be higher than in later years

- made tax effective superannuation contributions without diminishing concessional and non-concessional contribution limits

- Downsizer SMSF contribution provided efficient way to add to SMSF without diminishing concessional and non-concessional contribution limits

2. SMSF grew considerably, aided not only by good investment returns but also with regular tax effective contributions

3. Sufficient funds were available to assist children in home purchases

Investment – summary

David and Angela have a good understanding of the trade-off between return and the volatility/risk of those returns. They have the capacity and willingness to absorb volatility and accept the risk of price fluctuations, particularly over periods less than the minimum recommended investment time frame.

They understand that capital preservation cannot be guaranteed and are prepared to invest for a minimum of eight years.

So, what can First Samuel do for you and your small business?

Reclaim your time: Spend your time on what you enjoy and where you can make a difference, such as your family, business, friends and lifestyle. And take effective action.

Grow your wealth: And your business. At the very least, your wealth needs to grow at the rate that will provide income to replace your wage or salary when your wage or salary ceases.

Own your financial future: Have the capacity to cope with the planned and unexpected changes in your business and your life, and ensure that your financial objectives are still relevant.

The next steps

Call us and arrange an hour-long consultation with one of our Private Client Advisers and an investment manager.

There is no obligation and no cost.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.