© 2024 First Samuel Limited

Time is an asset of which busy professionals have little. Wealth management for professional women can help overcome challenges and build financial security.

Issues such as the gender pay-gap, disproportionate care-giver responsibilities, and a longer life expectancy all continue to impact women’s ability to save, invest and accrue wealth.

However, women who have a good income and outsource the management of their wealth can meet and exceed their wealth goals.

This is the third instalment of our five-part case study showcase. We focus on single professional women clients who have a high income and relatively lower capacity for risk.

Through this case study we once again focus on how true ‘Wealth management for professional woman’ is a blend of wealth strategy advice and individual investment management.

Successful Client Outcomes

Directorship complexities and surplus cash optimised

- Directorship investing constraint overcome

- Second portfolio to capture excess cash flow and unused pensions

- In-specie transfer from SMSF to family trust to utilise carry-forward losses

Our client

Rebecca is in her mid-60s, single and with two adult and independent children. She is a non-executive director of a number of public and private companies and government bodies.

She has little time to manage her own investments.

What she sought

- How to best invest and trade in shares of companies of which she is a director

- How to best invest her excess cash flow from employment and unused minimum pension

- Other sensible and tax-effective advice

Critical client facts

Financially, her more recent and key arrangements are:

| Item | Owner | Value | Comment |

|---|---|---|---|

| Home | Rebecca | $1.8m | No debt |

| Fees | Rebecca | $0.3m | Mainly director’s fees, some consulting |

| Securities | Rebecca | $0.2m | Companies of which she is a director |

| Cash | Family Trust | $0.01m | Trust has significant carry-forward losses |

| Securities | SMSF | $2.5m | |

| Retail property | SMSF | $0.5m |

What we advised – summary of wealth management for professional woman

- How and when to trade in the shares in companies of which she is a director and other exclusions.

- Draw only minimum pension benefits, to keep assets in the SMSF where the investment earnings are tax free.

- Establish a separate portfolio in her family trust, to manage unused pension income and other cash surpluses, and use carry forward losses to offset the tax that would otherwise be payable.

- When she retires, make a lump sum in-specie withdrawal from the SMSF and transfer to the family trust (i.e. a transfer of securities – hence no need to sell in the SMSF and use the cash to buy in the family trust), subject to a CGT assessment at the time.

What was special

- Rebecca met her directors’ duties and her desire to trade in shares of the subject companies

- She maximised her SMSF by keeping pensions to a minimum, retaining as much as possible in the tax-free pension environment

- She optimised investment of her surplus cash in a tax-effective manner by utilising a separate portfolio held by her family trust

- She would be in a position to lower the tax she would otherwise pay with the transfer to the family trust by using the trust’s and her own carry forward losses and her personal tax-free threshold

Investment

Client’s attitude to return and risk

Rebecca’s tolerance of the risk of a negative return in the short-term is low. She understands that short-term volatility may be greater for assets that produce higher returns in the longer-term. She is also comfortable having a lower risk portfolio with a preference for income-producing assets, although she has surplus income. The opportunity of capital gains is not as important as the avoidance of capital losses.

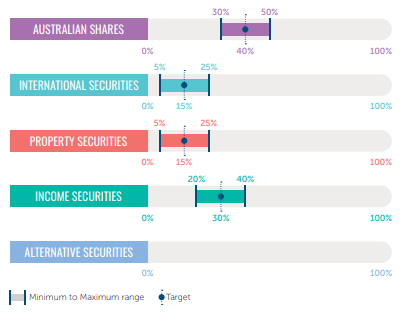

Asset Allocation: SMSF and Rebecca’s portfolio

Investment Programme – features

| Investment Objective | To outperform CPI by 3% p.a. after all fees and tax benefits |

| Assumed tax rate | 7.5% |

| Prohibitions | ‘Long-term’ investment such as private equity and venture capital |

| Income | Reinvested |

| Payments | Minimum pensions from the SMSF |

| Sector or security tilts | Nil |

| Other 1 | Note current directorships. Be alert for trades |

| Other 2 | Consolidate portfolios for fee calculations |

What was special

- Use of separate portfolios and entities in order to optimise her tax position

- Ability to direct trades in directorship companies

- Investment prohibitions were effectively replaced with securities of similar expected return and risk

Conclusion

Of our over 250 clients, we manage over 100 different asset allocations (i.e. the mix of Australian shares, income securities, etc) with up to six different security themes within. These themes are:

So we:

- tailor the wealth strategy advice that we give, both initially and ongoing

- design, build and manage highly bespoke investment portfolios

This supportive model helps our clients to overcome challenges, build wealth and achieve financial security.

How can we help you

Call us today and make an appointment to meet with one of our Private Client Advisers. There is no cost or obligation prior to your agreement. We’d like you to give us the opportunity to see how we can help you.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.