© 2024 First Samuel Limited

The Markets

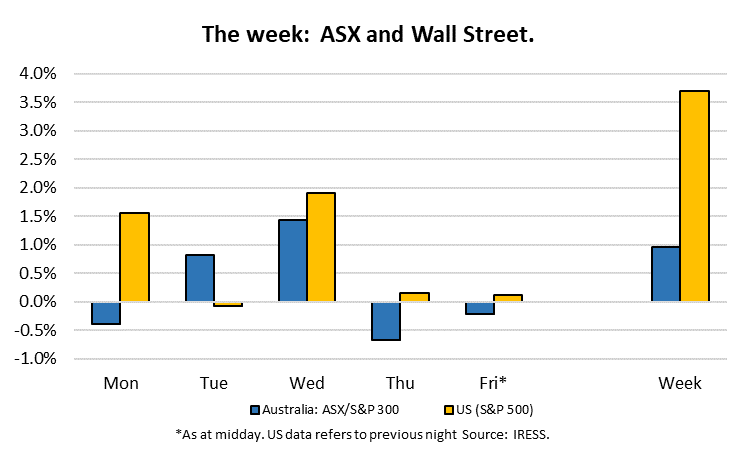

This week: ASX v Wall Street

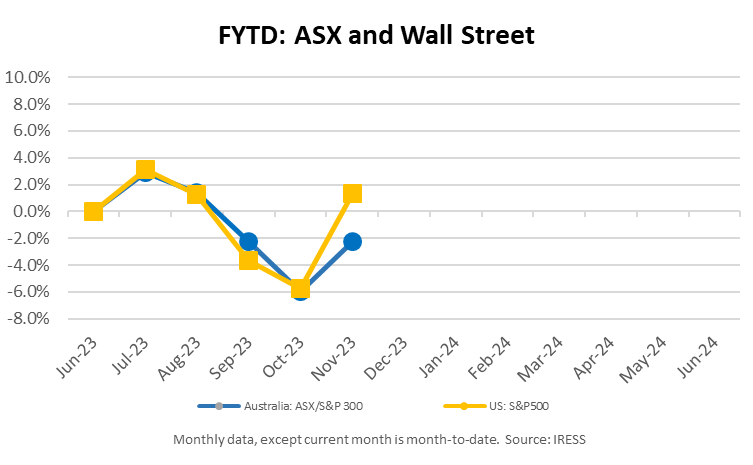

FYTD: ASX v Wall Street

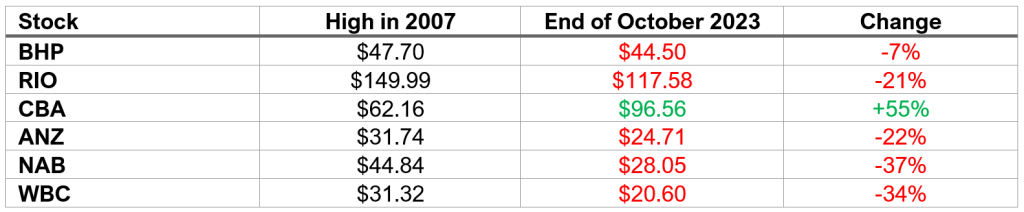

In recent weeks, we heard the mildly alarming statistics that the ASX had fallen to a low in October 2023 of 6703.2. This was lower than the levels seen in the broad market index at the close of October in 2007 (6770).

Indeed! Sixteen-plus years in which the market had no overall capital growth and only the benefit of dividends (albeit significant amounts and often fully-franked).

Some may throw their hands in the air and decry the weakness of equity investing. This would be a mistake. Picking the long-term peak that October 2007 represented and comparing this peak to a short-term low this year is a little unfair. But the more substantive impact that should be considered is “what companies drove such a sombre outcome?”

First Samuel’s recent CIO Dinner series was titled – “There Is More to Investing that BHP and the Banks.”

You may be surprised to know that the main drivers of the weak capital appreciation in capital between 2007 and 2023 came from the two large miners, BHP and RIO, and three of the four major banks.

The table below highlights the share prices of these six companies in 2007 and 2023.

The remainder of the market outperformed in terms of capital growth.

Rebounding markets

Having noted the weak historical performance above, we need to follow up with news of the significant rebound in markets since the end of October.

The broader index (ASX300) is up 4.6% in November following an equally weak October. Smaller companies have rebounded 5.8%, reversing a similar loss in October.

As we noted in a recent commentary, we had believed that the sell-off in late October was an opportunity to purchase shares with not only the cash we have saved for better value, but also some the proceeds from recent takeovers.

We are pleased to have completed some good buying in late October and early November.

Nufarm FY23 Financial Results

Background

Nufarm is a global crop protection and seed technology company that develops and manufactures crop protection solutions.

Its key segments are North America (36% of FY23 revenue), APAC (28%), Europe (25%) and Seed (11%). Key products include non-selective herbicides, other selective herbicides, phenoxies, fungicides, seeds, insecticides, and a range of specialty products.

As noted in the recent CIO Dinner series, Nufarm is a company that is adapting to new sources of advantage with its seed technologies business. In response to changing dietary and nutritional needs globally, the company has developed a range of seed solutions that promise to generate significant value in the long run. We see possible outcomes in which the Seeds business is worth almost one-third of the total company’s value.

Weak short-term global conditions in the industry over the past 12 months have provided clients with an opportunity (since July 2023) to buy Nufarm at what we believe represents a significant discount to underlying value. Global issues have included channel destocking (excess supply), which impacted volumes and led to wholesale price declines. We are confident that these conditions are short-term in nature.

The combination of patience to look through short-term conditions and expected increases in the value attributable to the seeds business is appealing.

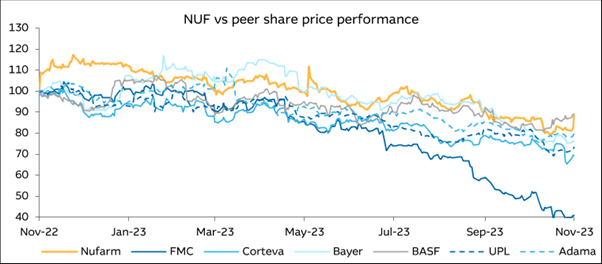

The FY23 results released on Thursday highlighted that despite tough conditions, the company has performed better than its global peers. It delivered more robust than expected cash flow and an operating earnings result (EBITDA) that was only 2% cent lower than FY22.

Due to this stronger performance, the sell-off in Nufarm (-11%) over the last 12 months has been lower than the peer average of -30%. The chart below compares the share performance of Nufarm versus these global peers.

The stock price was up 5% since the beginning of the week.

Long-term issues and opportunities

We were pleased with several structural features of the result, including.

- Reinforcing the value of the company’s extensive product development pipeline in Crop Protection

- Several new product launches and registrations during FY23 spread across biologics, synthetic crop protection and adjacent solutions

- Good working capital management

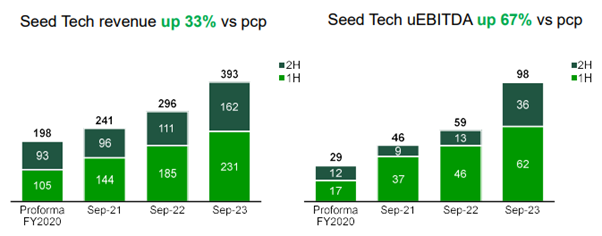

- Management reiterated confidence in stated long-term targets for 2026. Nufarm targets group revenue of $4.6bn in FY26, up from $3.5bn in FY23 and $600-700m rev from Seeds by FY26, versus $393m in FY23.

The upside from current levels is considerable for two core reasons.

- We believe the Seeds business is worth a significant premium to the current implied value. This can be unlocked by delivering on expectations or through M&A – either a sale or a demerger of the business. Transaction for similar seeds businesses suggest a significant premium is possible. The growth and profitability of Seed Technologies is clear in the two charts below.

- The company continues to trade at a discount to each of

- Our bottom-up valuation

- The remainder of the larger capitalisation companies on the ASX

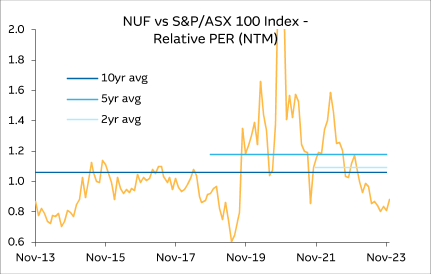

- The company own history of price-to-earnings ratio. The chart below shows a chart of the relative PER (price to earnings ratio) highlighting in yellow the discount to the market (circa 0.8), and versus its average relative price over the past 10 years of 1.06. Were this to simply correct to long-term levels there is at least a 20% return.

What the market said

“A solid FY23 set against low expectations with Seeds and gearing/cash flow better than consensus. With seeds earnings growth now coming through & FY26 getting closer, we think the market is likely to focus more on Seeds earnings & valuation upside”.

Aristocrat FY23 Financial Results

Background

Not all clients will hold Aristocrat Leisure, depending on the nature of individual client restrictions. For those that do it is a substantial position in the Australia Equities sub-portfolio.

Aristocrat Leisure started out as a slot machine manufacturer and developer of poker machine gaming content. It started in Australia and expanded to its key market in North America, where it is the leader in gaming operations.

Over the past decade, Aristocrat has broadened into other verticals, including digital (Pixel United), underpinned by three acquisitions, which allows it to serve content into the social casual and social casino segments. Social casual refers to the range of mobile-based games that the world has increasingly become enamoured with as we spend more time on our smartphones.

The capacity of Aristocrat to take its expertise in developing games, once confined to the pokies’ venue or casinos, to other formats has generated significant value. In addition, the strong cash flow generation characteristics of the company have meant that Aristocrat has been in a prime position to acquire companies and their expertise to complement historical product development.

Pixel United, Anaxis, and the yet-to-be-completed the acquisition of NeoGames all represent examples of acquisitions that have added to the vast capability of Aristocrat across the range of products, technology, systems, and marketing of gaming products.

Highlights from the result

There were a range of technical and company specific aspects of the result that were pleasing to our detailed modelling of Aristocrat’s valuation. Volumes of machine sales, improvements in the profitability metrics of social gaming, and the fabulous outcomes achieved in terms of market share in the US casino market were all impressive.

What we would like to highlight in this review is the longer-term features of the result.

We love investing in companies that can achieve the following “classic trio of performance:”

- Strong growth in revenue – up 13% on FY23;

- High levels of cash generation, – especially with respect to overall balance sheet strength; and finally

- High level of investment to sustain and provide future growth and market position.

We tend to see such a “trio” in classic strong performers such as Woolworths or Seven Group Holdings.

Aristocrat, in this result, reinforced the power of its business model to ramp up investment from a position of strength.

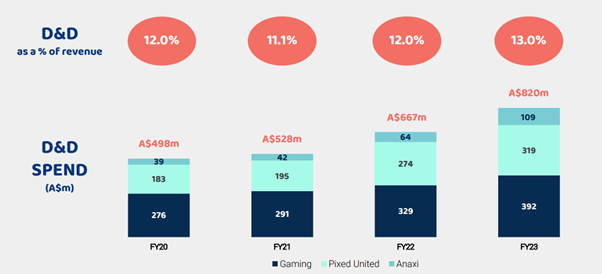

Analysts noted that “FY23, and especially 2H23, proved to be a turning point where the rate of organic investment lifted after years of decline. Sitting behind this was;

- a big step-up in capex including A$280m in 2H23, more than the whole of FY22, partly driven by the record ops growth;

- higher Design and Development (D&D) spending at A$820m, up 16% in USD and at 13% of sales (above 11-12% guidance). It was the highest rate recorded since FY14 and included.

- +A$63m in Gaming,

- +A$45m in Pixel (social gaming) and,

- +A$45m building Anaxi (technical development)

The following chart shows the increase in investment (as % of sales) that the company has pursued since FY20. Considering the scale of the business ($6.2bn in revenue), the commitment to spend such a large share on revenue of research and development is a credit to management and to the scale of opportunities the business sees for future growth.

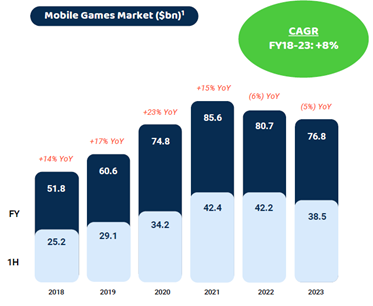

What is social gaming?

As CIO, I am conscious that many readers may not be aware of exactly what social gaming is, other than it being revenue collected from a series of games played on the mobile phone (or online). Many readers may spend some time playing games on their phones, but I suspect that fewer would pay to play such games.

However, one’s reluctance to undertake such pastimes shouldn’t obscure the size of this market, which reached a peak in the Covid period. The chart below shows total global spending $76bn USD.

Some of the revenue is simply the mobile phone version of land-based casino games, but the remainder is an entirely new form of global entertainment.

Pixel United, the social gaming arm of Aristocrat generated $2.6bn in revenue in 2023.

A game called EverMerge, generated USD$400m in revenue alone.

What is EverMerge?

“EverMerge is a magical world that gets bigger and better with each discovery. Come play this part merge, part world-building puzzle game. EverMerge’s sandbox-style play offers endless possibilities and combinations! Find new mergeable items – and meet classic characters and creatures – as you complete puzzle quests and reveal new lands.”

The profitability of such games can be astounding once they have been created, and have developed sufficient following, critical mass, and targeted marketing investment strategies.

Pixel United overall tends to make the follow indicative profits from each $1 of revenue. It pays away up to 30c of revenue in commissions (e.g. the share to Apple), spends 20c+ on marketing to generate new players, only around 10c in the cost of operating the game – leaving at least 30c or 30%+ profit margins.

The combination of the outlook for future growth, the strong current profitability and the depth of capacity that Aristocrat has developed results, means social gaming is a significant portion of our valuation for Aristocrat.

What the markets said (Macquarie Equities):

“The outlook for earnings upgrades is promising, with our forecasts yet to include revenue synergies from the NeoGames transaction, with Aristocrat likely to move quickly on distributing content. We also hope to see margin benefits in Pixel United, with the launch of a social casino direct-to-consumer platform in FY25.”

Summary

In summary, we were pleased with both the execution of existing strategies and excited by the scale of the new investment. With the NeoGames acquisition expected to be bedded down in the coming 12 months we see continue upside from current price levels.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.