")

© 2024 First Samuel Limited

Sovereign risk is the risk of a country or state failing to meet its debt repayments or obligations.

The Short Story

Are there significant sovereign risks to wealth for Victorian residents?

Probably not…

- Current plans for tremendous population growth will underwrite the state’s finances

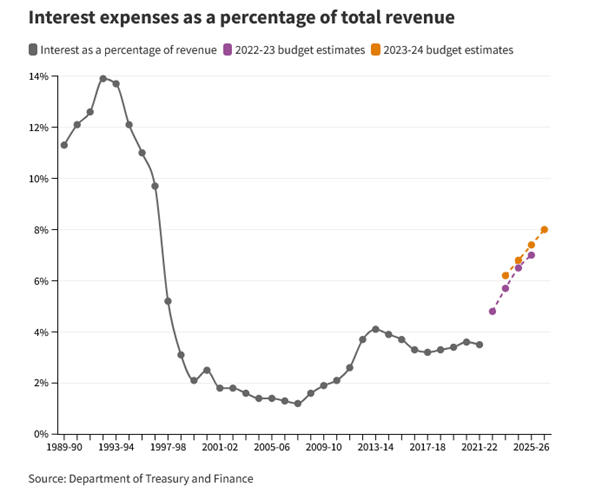

- Current budget conditions are not yet critical – servicing costs are moderate (reaching 7% in 2025) versus a revenue growth rate, and growth in the nominal economy of a similar size

- The government’s credit rating remains strong: AA with a stable outlook by Standard and Poor’s and Aa2 with a stable outlook by Moody’s Investors Service

But…

If the state’s finances deteriorate, Victoria possesses a considerable range of existing and possible future growth taxes – payroll, land, and location-based taxes.

Victoria might also be the beneficiary of federal government munificence, as exemplified by yesterday’s housing announcement.

Irony

The irony is that Victoria needs to invest even more to provide amenity to the expected increased population growth.

Should Victoria fail to invest, higher public transport and health care costs will be the most significant risks to the cost and quality of living of families and individuals in the middle of the income wealth scale.

For the poorest, additional support will be likely: it will be delivered by governments and institutions charged with such a role.

For the wealthiest, the total cost of these services remains a relatively minor burden, especially expressed as a percentage of wealth.

But those without either significant wealth (e.g. a non-primary residence) nor access to support, will face the most significant burden when health and transport costs rise in the face of lower government support for such services.

The Longer Story

Are there risks regarding Victorian’s quality of life?

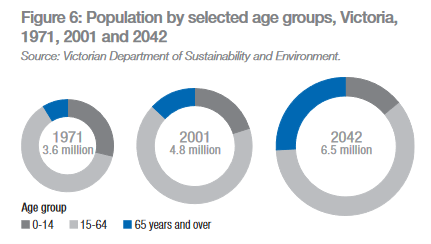

Certainly, yes. The Victorian government has changed its original plans for slower growth. In 2018, Victoria’s population surpassed its original 2042 projection!

The past decade of student and grandparent migration has vastly exceeded expectations. New plans anticipated further growth.

The Victorian government assisted (and coordinated with) the federal government policy on this population-led growth agenda, which is the key to understanding government policy.

Our most significant sovereign risk will emerge should the anticipated population not arrive.

We believe that the Victoria government and its policy and planning will sacrifice its residents’ quality of life to further concentrate the economic advantages and quality lifestyle outcomes in a narrow range of locations.

Should we choose other than population-led growth, the sovereign risk to existing wealth abounds.

Sovereign risk

Sovereign risk to wealth, highlighted by recent budget and political experiences, including the decision to abandon the 2026 Commonwealth Games, has two clear forms going forward.

What if the migrants don’t arrive?

With a lower-than-forecast population, the same increase in investment and debt would be required to maintain growth. This would mean the higher costs being spread amongst relatively fewer residents. The funding costs per capita increases, necessitating new taxes being levied.

What if debt servicing costs increase?

This occurs if the rest of the world loses faith in the state government’s capacity to service our existing debt or seeks a higher rate of interest on future debt raised.

So, regardless of population growth, the cost of servicing debt rises, creating the need for higher per-capita taxes.

Four outcomes

Possible outcomes of the above nature would include:

- Increased wealth taxes, especially levied on land ownership. These currently attract lower taxation than other activities in Victoria.

- Reduced investment will reduce the quality of life but not attack wealth directly.

- Increased government, quasi-government, or formerly government-provided goods and services costs.

- Alternative funding sources are required to fund investment. In the short run, the state government has a limited range of taxes and charges it can levy. However, in the long run, the interplay between the federal government and states, especially regarding wealth and superannuation, may need to be reimagined.

Population growth is the key to understanding sovereign risks

In 2004, Victoria’s population was expected to reach 6.5m by 2042, by which time population growth rates (percentage per annum) were suggested to have halved. See below.

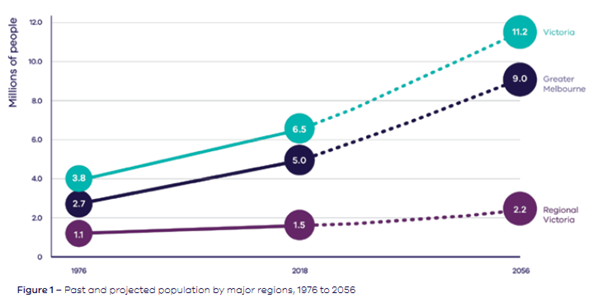

This all changed in the decade to 2019, and following a hiatus around covid, explosive growth is now the core forecast on which policy (including finance) is predicated.

Two paradigms are possible with the level of population growth.

- Population growth is delivered at the expense of quality of life, real income, or real per capita output considerations.

- Population growth comes with productivity-led wealth creation. However, this only comes with:

- Microeconomic reform

- Transport reform

- Significant technological innovation

- Very highly skilled migration – as opposed to current forms

The geographical and planning consideration of such a level of population growth, on which budgets are created, are yet to be considered from a physical or infrastructure perspective. No geographic distribution of population growth in population past 2036 has been contemplated – it is simply too tricky.

The population in December 2022 was 6.7m. But this failed to include more than 300,000 temporary residents, including students and illegal workers. With extra population constrained within the same area, the location rents (value of services available) will only grow.

Determining where and how people live requires some ideas about where they will work and what level of distortion in value is possible between the importance of living in, says Portsea versus Drouin East.

Should current patterns persist, this gap could be huge. And the benefits will accrue very rapidly to a relatively small number of people. For instance, travel times to some parts of Melbourne will rise rapidly, and others with the benefit of existing public transport built more than a century ago find little change.

Similarly, places with a comparative excess of existing health services or educational institutions gain further in relative terms as new growth areas or existing areas with rapid density increases fail to keep pace.

How does the Victorian Budget work – is it a source of risk?

As you can see, most of state-based revenue comes from ‘growth’ taxes. That is, from population or economic growth.

Notions of a perilous budget are usually predicated upon issues that include:

- Lack of growth-oriented taxation

- High structural deficits

- Existing debt that is too high

- High-interest rates charged on outstanding debt

At this stage, the growth orientation of existing taxes is acceptable; structural deficits are moderate given future growth, the outstanding debt is reasonable considering the budget size, and the debt cost is still cheap despite recent rises in rates.

In a growing economy with significant control over its income, debt levels at 23% of Gross State Product are manageable.

The sustainability is further enhanced by current projections, which see future deficits becoming smaller.

Payroll taxes

With massive population and moderate inflation, the growth in payroll taxes will continue to exceed growth in nominal GSP, primarily if real wage growth is delivered.

At this point, a little math is required. There does come a point at which the level of debt is so high that wages growth (and with that payroll taxes) cannot keep up. We are not yet at this point. In fact, we remain at the point at which wages growth improves the government budget position on a standstill (i.e. no change to policy) basis.

However, payroll taxes are particularly egregious in an open trading economy: they tend to reduce demand for labour, reduce competitiveness and burden new firm creation with higher barriers to entry. To assuage some of these concerns, smaller businesses are usually spared. Recent changes to payroll taxes in Victoria have concentrated on large national companies paying the most, which makes sense.

The problem with the Australian industry is that it isn’t particularly competitive and suffers considerably from oligopolistic industry structures in areas including finance and insurance, supermarkets, and telecommunications providers.

In these circumstances, the imposition by one state of higher payroll taxes is unlikely to have any significant impact other than on marginal investment, average wages, or profits. Woolworths will still have just as many supermarkets, Suncorp won’t stop selling insurance, etc.

Fines and gambling

Fines and gambling taxes can be continued to be expanded with abandon. Victoria is the highest fining state already, yet when one considers all of the places in which charges can be levied, fines for breaking more minor laws and policies are attractive; to this author at least.

Twice the growth

Eventually, we return to the “two paradigms problem.” After signing up for twice the growth in population numbers per year than the previous 30 years, the principal budget risks are that the growth driven by the higher expected population isn’t delivered. Although there remains a risk of higher interest servicing costs, quite often this risk is reduced if economic growth is high, even if that economic growth is purely population-led.

The level of growth-oriented taxation is plentiful in the Victorian budget. It could easily be expanded to a range of additional services, higher fines, and fees with limited impact on the cost of living.

Housing problem

The most significant opportunities for higher levels of taxation would relate to the dramatic need to alter the housing distribution within the state should Victoria reach an 11m+ population level.

The total cost of providing services to stand-alone housing, especially as it is likely that more than 30 percent of this housing will have a single occupant, will be prohibitive.

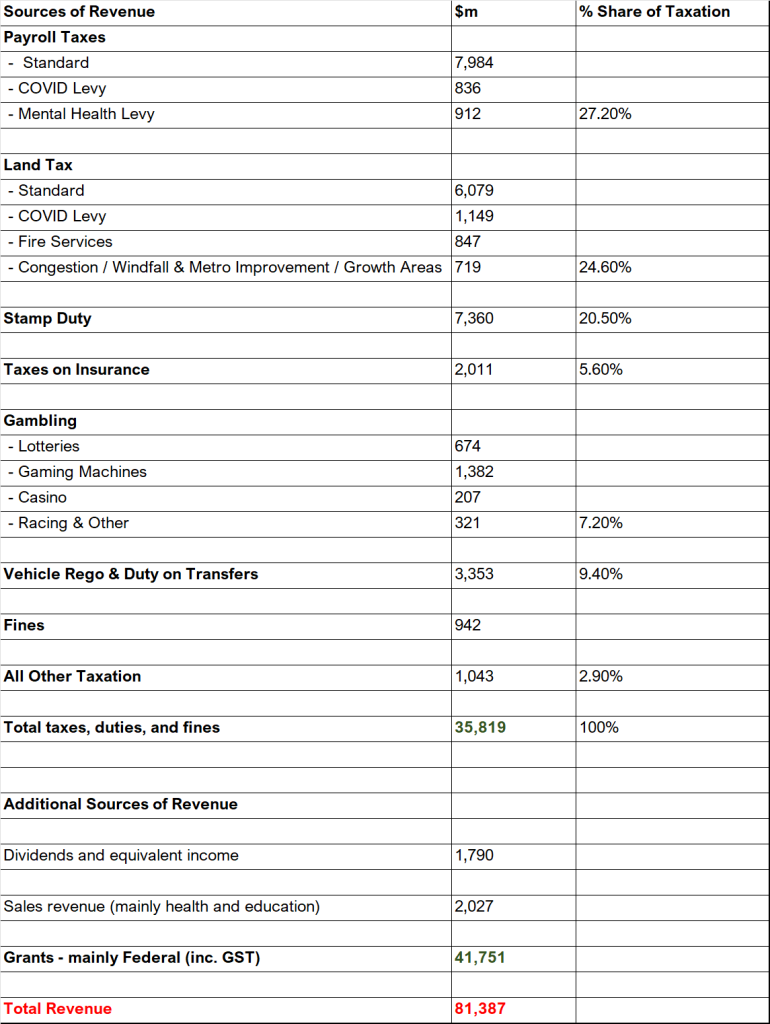

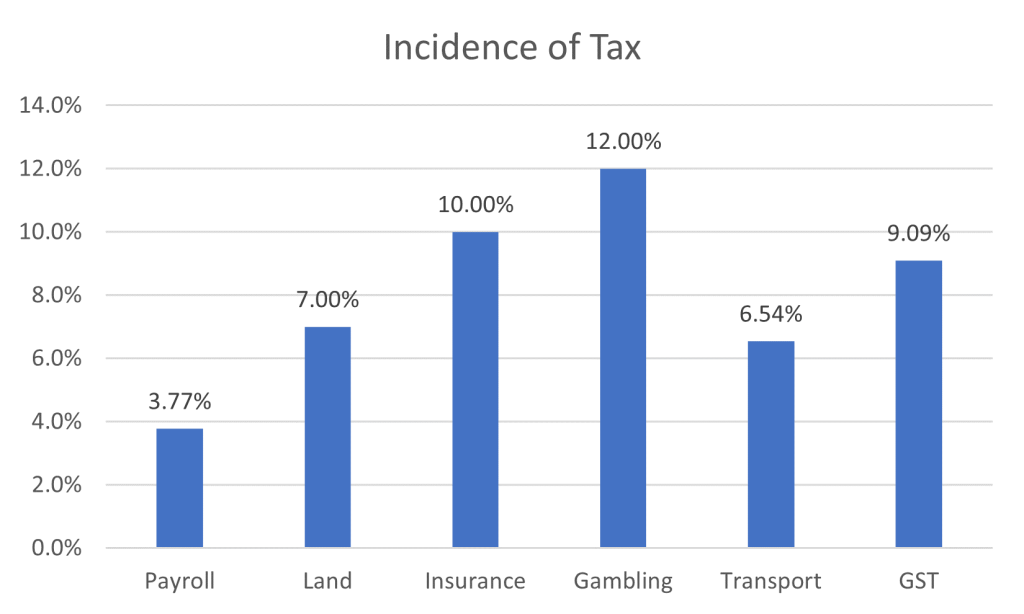

The following chart outlines the incidence (in the percentage of income/spending terms) of currently levied taxes.

Of the most output-limiting taxes, payroll taxes are the least taxed in percentage terms. The highest taxed is gambling. And of course, the GST is 9.1% but not applied to all expenditures.

The least taxed activity other than employment is land ownership, which also is the beneficiary of the largest subsidisation in the federal budget (negative gearing, capital gains discounts, principal residence exemptions in social welfare, etc).

In the absence of a range of taxing powers that only the federal government can access, it would be intuitive to imagine that a range of annual taxes, such as taxes on the principal residence replace stamp duty as mooted in NSW and ACT.

We note that such a change remains one favoured by economists, as it would be an efficient source of additional revenue to smooth out the impost of stamp duty on the young.

What is clear, however, is that the uneven pressure on land and property taxes will only be exacerbated if the principal residence remains tax-free. This is best seen in the reliance on development taxes, urban growth boundary levies, and inner-city parking levies, which desperately try to grow the total take on the property.

Importance of innovation and development

An area that provides the author with increased confidence in the finances is the role of technological innovation. There are five reasons why such optimism may prove critical:

- Energy and electrification revolution. Pure population growth, i.e. simply adding extra people organised the same way as the day before, is expensive and lacks numerous productivity drivers. Population growth enables changes in investment by partly defraying the costs to original inhabitants but has little scope for effective change.

- Australia requires considerable energy reinvestment to benefit from any move to Net Zero by 2050. Delivery of this scale of incremental investment will be supported by the scale of investment required for the population growth alone.

- Higher levels of population growth will reduce this investment’s marginal per capita cost and may also provide productivity enhancements if well planned.

- Geographic reorganization enabled by innovation.

- Changes in workforce engagement patterns.

Transport

The most significant issue for productivity after technology and innovation will be transport.

Without one of the following, Melbourne can simply not hold the 9.0m people suggested by 2056 plan:

- Massive reorganization of mobility tasks within the city, including the build and adoption of the Melbourne Suburban Rail Loop

- The delivery of the third national/international airport near Cardinia

- Dramatic reduction in surface freight travel and the expansion of the Port of Hastings

- New ways to house older single households, which currently and on official projections continue to remove options for the supply of built form for families

Should Victoria fail to invest, higher public transport and health care costs will be the most significant risks to the cost of living of families and individuals in the middle of the income wealth scale.

For the poorest, additional support will be likely: it tends to be delivered in by institutions and policies charged with such a role.

For the wealthiest, the total cost of these services remains a relatively minor burden, especially expressed as a percentage of wealth.

But those without either significant wealth (e.g. a non-primary residence) nor access to support face the most significant burden when health and transport costs rise in the face of lower government support for such services.

Conclusion

Victoria, or at least its political elite, has chosen a growth orientation heavily dependent on historically elevated rates of population growth.

This population growth will reorient activity and generate significant social change, from which there will be a range of winners and losers. One beneficiary will be the Victorian Treasury, which will continue to benefit from this type of nominal overall growth. In turn, current pressures on the budget, and the levels of outstanding debt will begin to be relieved despite funding the huge amount of investment in fixed and social infrastructure that will be required.

Taxes are likely to rise, but we suspect such taxes will remain relatively benign with respect to wealth. Indeed, the funding requirements of the state may create additional investment opportunities in the medium term.

Could Victoria have chosen a different path? Perhaps. Yet, on our analysis, alternatives are becoming less likely to be enough. Victoria now needs to avoid half measures, where the promise of short-term relief removes investments that are only vital today but will be critical tomorrow.

Read last weeks Wealth intelligence.

The information in this article is of a general nature and does not take into consideration your personal objectives, financial situation or needs. Before acting on any of this information, you should consider whether it is appropriate for your personal circumstances and seek personal financial advice.